Vienna Faculty Op-Ed: The Ramifications of the Russian-Ukraine Conflict to the World Economy

March 22, 2022

In their recent commentary, Dr. Menbere Workie Tiruneh, Associate Professor - Finance and Economics and Dr. Nikolaos Antonakakis, Associate Professor and Area Coordinator for Economics and Finance at Webster Vienna Private University, attempts to explain what’s at stake for the global economy as conflict looms in Ukraine. However harsh the effects, the immediate impact will be nowhere near as devastating as the sudden economic shutdowns first caused by the coronavirus in 2020.

With the exception of the Balkan wars in the 1990s, Europe has been largely at peace since the deadly World War II that took the lives of an estimated 75 million people on earth. The ongoing conflict between Russia and Ukraine is undoubtedly a major turning point with significant and multifaceted implications not only for the European peace and security but also for the world economy at large.

Estimating the global macroeconomic ramifications of the Russia-Ukraine conflict is not an easy task to accomplish due to continuously rising sanctions against the Russian economy and the uncertainties on the scope and scale of the conflict in the months to come. Nonetheless, the ongoing conflict is undoubtedly a major blow to the global economy that has been struggling with the consequences of the global lockdown measures following the Covid-19 pandemic, and represents a significant setback for the hope of a swift economic recovery.

Before embarking on the analysis of the impact of the Russia-Ukraine conflict on the world economy, it is necessary to take a snapshot of the two countries’ significance for the world trade. Russia and Ukraine represent important exporters of commodities and both are significantly integrated into the world economy. It is well known that Russia is the third largest producer of oil. Russia exported nearly 5 million barrels a day of crude oil in 2020, according to the U.S. Energy Information Administration. Given the geographical proximity and in line with the gravity model of international trade, Russia and Ukraine are highly integrated with the EU’s economy as well. Russia represents EU’s fifth largest trade partner, accounting for 5.8% of the EU’s total trade in goods. According to the European Commission report, in 2020, “the EU was Russia's first trade partner, accounting for 37.3% of the country’s total trade in goods with the world. 36.5% of Russia’s imports came from the EU and 37.9% of its exports went to the EU”. In monetary terms, the total trade in goods between the EU and Russia totaled €257.5 billion (European Commission, 2022).

While smaller in scale, Ukraine’s trade with the EU is also significant. According to the European Commission, Ukraine was the 17th largest partner for EU exports of goods (1.3 %) and the 15th largest partner for EU imports of goods (1.1 %). Russia and Ukraine are also some of the largest producers of agricultural commodities, such as wheat and corn. For instance, the combined wheat export of the two countries accounts for approximately 25% of the world export of wheat.

In economic impact assessment, bilateral trade is measured based not only on the size of bilateral transactions, but also by the scale of dependency and the availability of substitutes when the system encounters exogenous shocks.

What are the key economic and financial sanctions against Russia?

The sanctions against Russia are described as historic and unprecedented. In economic terms, imposing stringent trade sanctions on Russia is particularly a painful policy choice to European policymakers due to the overwhelming impact of such measures on the European economy that is highly dependent on energy imports from Russia, which accounts for 62% of EU’s total energy imports (equivalent to €99 billion). Compared to the EU, other large size economies have a more moderate dependency on the Russian energy market. For instance, the U.S. imported about 8% of its oil and refined products from Russia in 2021; while China imported more than 15% of its oil imports from Russia during the same year. The U.K. imported nearly 4% of its gas from Russia in 2021.

As stated above, in an intertwined global commercial and investment landscape, impact assessment based purely on bilateral trade ties won’t be informative due to spillover effects. For instance, even if Russia-China bilateral trade won’t be affected by sanctions, trade and investment disruptions between the world and Russia will still have negative spillover effects on bilateral trade between the world and China, since China is one of the most important trade partners to the world. Hence, when a country or a group of countries impose sanctions on their vital trade partners, it also implies imposing a partial self-sanction. The negative impact is clear when one looks at the degree of dependency of the EU on imports of petroleum and natural gas on Russia (mentioned above), which is yet not part of the new trade sanctions, because of its crippling impact on EU economies.

Overall, the sanctions imposed on Russia can be summarized into three main areas. The sanctions targeting the financial system can be considered as the most painful to the Russian economy. The reason is that when foreign assets of a central bank and other banks are frozen, this will prevent the central bank from using its large foreign exchange reserves - considered a vital monetary policy tool - to support a domestic currency to sustain the pressure of devaluation. As a result of these sanctions, the Russian rubble lost 30% of its nominal value against the U.S. dollar, and to prevent further pressure on its currency, the Russian Central Bank raised its nominal interest rates from 9.5% to 20%. This has been followed by other measures, such as imposing limits on foreign-currency deposit outflows and temporarily suspending dividend and interest payments to foreign shareholders and creditors, among others. As part of the financial sanctions, removing Russian banks from the Society for Worldwide Interbank Financial Telecommunication (SWIFT) implies that these banks will not be able to settle payments in foreign currencies to their clients. This hampers trade and significantly reduces Russian ability to service its foreign-currency denominated external debt. Other sanctions include trade and investments, which also triggered the departure of numerous financially influential companies from Russia. Closing EU’s airspace for “Russian-owned, Russian-registered or Russian-controlled aircraft” has significantly hampered the export of goods and increased transportation and other transaction costs. This of course is expected to deteriorate Russian trade balance and increase both inflation and unemployment. On the other hand, since the energy sector has been exempted from sanctions, Russia still manages to collect the vital foreign exchange revenues thanks to rising global energy prices.

How will the Russian-Ukraine conflict affect the world economy?

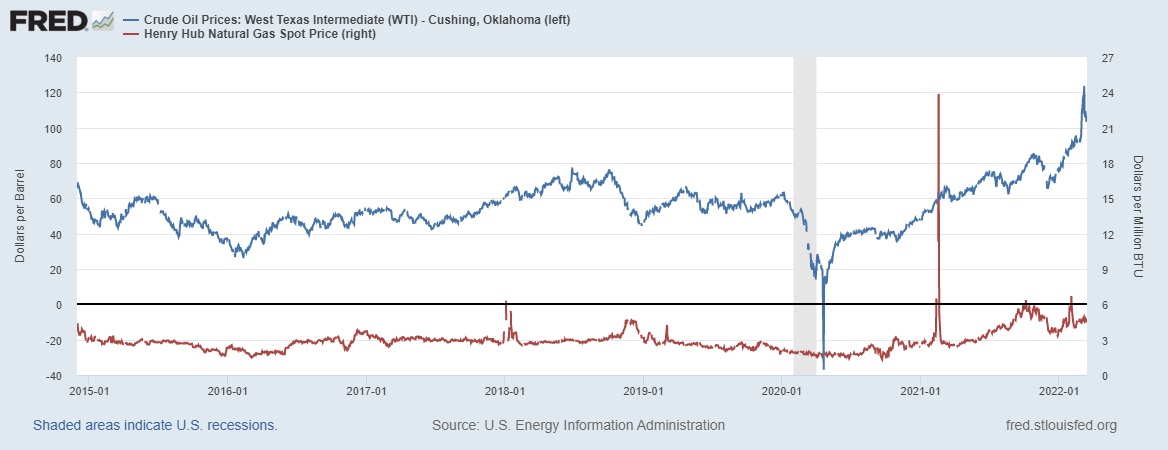

There are various channels through which the Russia-Ukraine conflict can spillover to the rest of the world economy. The first impact is observable by soaring energy (crude oil and gas) prices, as shown in Figure 1, which can decrease global consumption and investments, and slow down the world economic growth. Higher energy prices often lead to higher prices for other goods and services. Consequently, inflation has already been on the rise in advanced, emerging and developing economies. The recently released US inflation report, which is estimated at 7.9%, is considered as the highest inflation rate in 40 years. Due to fear of energy supply from Russia, Euro Area inflation rate increased to 5.8% in February up from 5.1% in January 2022. However, it should be admitted that inflation was on rise even before the start of the Russian-Ukraine conflict. Albert Einstein put best, “you can’t blame gravity for falling in love”. As inflation expectations increase, major inflation targeting central banks, such the ECB and the FED, could proceed with interest rate hikes to bring down inflation back to its target. This in turn, however, will lead to a lower global economic activity, due to the increased cost of borrowing, resulting into a sluggish recovery to the already stagnant activity since the inception of the Covid-19 pandemic.

Figure 1: Oil prices (left axis) and Natural Gas prices (right axis)

Notes: Missing observations refer to non-trading days (i.e., weekends).

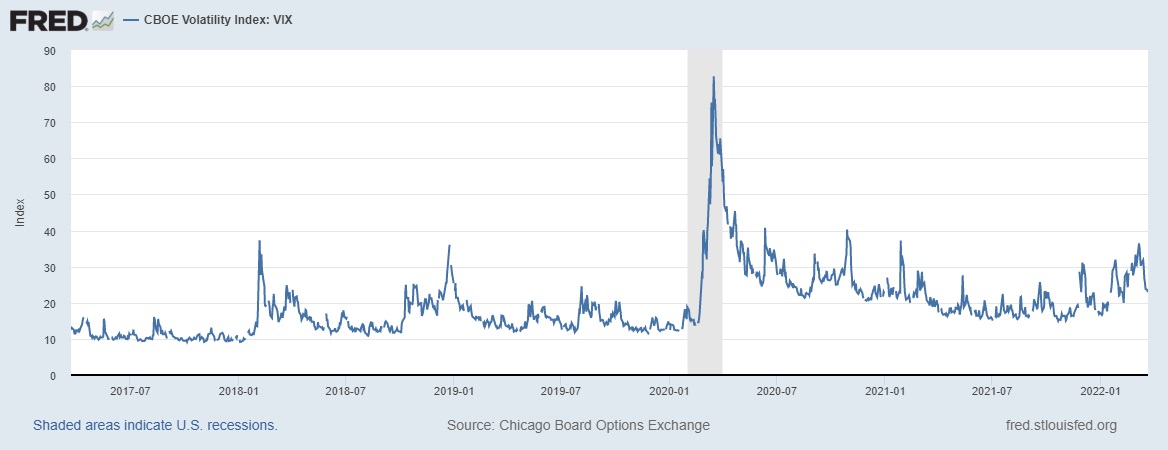

Figure 2: VIX

Notes: Missing observations refer to non-trading days (i.e., weekends).

The Russian-Ukraine crisis also increased the global volatility index (VIX), as shown in Figure 2 below, which serves as a measure of uncertainty or fear in the financial markets. As a result, there was a worldwide decline in stock prices. There is also another important channel through which prices could rise even more. Russia and Ukraine represent a significant part of the global supply of wheat, corn and fertilizer and the disruption of such commodity production implies lower supply, leading to higher food prices. As a part of the global consequences, this effect is predicted to be most severe in the Middle East and Northern Africa, which are most reliant on grain imports from Ukraine and Russia.

Adding fuel to the fire, the shortage of fertilizers would also imply important setback in production of food crops in other parts of the emerging and developing world. According to the Fertilizer Institute (2022), Russia belongs to one of the major producers of fertilizers, accounting for 23% of ammonia, 14% of urea, and 21% of potash, as well as 10% of processed phosphate exports in the world. Lower supply of fertilize implies lower agricultural productivity in emerging and developing countries. Sanctions against Russia by the EU and US and other countries and Russia’s retaliatory sanctions against its key trade partners would also imply overall decline in world trade, production and employment. As mentioned, EU’s decision to shut down its airspace makes transaction costs of exports and imports from and to Russia not only more expensive but also extremely slow. The longer the war lasts and the deeper the impact of existing and additional sanctions get, the more likely it is for the world economy to sink into a possible recession with multifaceted macroeconomic and social ramifications. As Mahatma Gandhi stated “An eye for an eye makes the whole world blind”.

About Authors

Dr. Menbere Workie Tiruneh, Ph.D., is Associate Professor of Finance for the Department of Business and Management at Webster Vienna Private University, and a part-time senior researcher at the Institute of Economic Research of the Slovak Academy of Sciences. Before joining WVPU, Menbere Workie served as International MBA Instructor for more than 10 years at City University of Seattle, European Graduate Programs.

Dr. Nikolaos Antonakakis, is Associate Professor and Area Coordinator for Economics and Finance at Webster Vienna Private University, as well as a Visiting Fellow at the University of Portsmouth. He had previously held a position of Assistant Professor of Economics at the Vienna University of Economics and Business (WU Wien) and at the Johannes Kepler University in Austria, and Senior Lecturer in Economics and Finance at the University of Portsmouth.